R3 IS SHAPING THE FUTURE OF REGULATED MARKETS

Enabling an open, trusted, and enduring digital economy where value is securely exchanged

Discover R3’s Corda, the leading tokenization platform powering the digitalization of real world assets and currencies for global regulated institutions everywhere.

live digital bond issuance on Euroclear’s D-FMI platform (powered by Corda)

bank in the world (HSBC) to offer tokenized gold (powered by Corda)

in Gartner’s 2023 Hype Cycle for Tokenization, Layer 1 blockchain platforms and smart contracts

digital bond issued on a Corda-powered exchange (SDX)

wholesale CBDC to support on chain settlement of primary issuance on digital exchange (SDX) powered by Corda

cross-chain repo swap PoC successfully completed with HQLAx (Corda) and Fnality (Hyperledger Besu)

permissioned enterprise DLT platform built from the ‘ground up’

green blockchain platform based on peer-to-peer consensus mechanism

to develop a blockchain platform that meets NIST cryptographic standards

Digital trust, delivered

The Collective Power of 3, only from R3

Distributed Ledger Technology

R3’s Corda is trusted by regulated institutions to enable tokenization of digital assets and currencies, faster settlement, and automation of complex business processes. Battle-tested by regulated networks operating at scale, Corda is the leading DLT platform for financial services.

Open, Connected Networks

Corda lays the foundation for interoperability, while CorDapp users can exchange value from one Corda network to another with privacy, security and control. R3’s blockchain ecosystem also enables you to tap into a diverse network of firms from the public and private sector.

Regulated Markets Expertise

R3 has a deep knowledge of financial services and collaborates with the industry to help accelerate the development of connected distributed solutions. Our Professional Services team has designed, developed and deployed hundreds of live CorDapps.

featured resources

Expert insights to guide your digital transformation journey

Blog

R3 caps off 2023 with record number of worldwide ‘firsts’, awards and accolades

Press release

Corda powers first digital bond issuance on Euroclear’s Digital Financial Market Infrastructure

op-ed

Can digital currencies give us the same freedom as cash?

blog

Gartner Recognizes R3 as Top Vendor in Tokenization, L1 Blockchain and Smart Contracts

video

Meet the next generation of Corda

resource hub

Interoperability Hub

The latest insights, use cases and resources on enterprise blockchain interoperability

Blog

Introducing Harmonia, a Hyperledger Lab: Unlocking interoperability

Blog

Agreeing to Disagree: Interoperability in a World Without Compromise

REPORT

The future of financial liquidity: CBDCs and Automated Market-Making

RESOURCE Hub

Digital Assets Hub

The latest insights, use cases and resources on digital assets

Resource Hub

Digital Currencies Hub

Expert insights, best practices and resources on CBDCs and stablecoins

TRUSTED PARTNER TO ORGANIZATIONS IN REGULATED MARKETS

Leading institutions rely on R3s Corda for the secure transfer of data, automated workflows and to tokenize assets securely

Financial services

Corda is widely recognized as the best-in-class platform for financial services because it is permissioned by design, scalable and purpose-built for high-value transactions.

Technology leaders

Technology leaders across regulated markets of all sizes and areas of expertise are benefiting from R3’s tokenization platform, Corda—whether it’s development of innovative new offerings that can connect and open up new markets for their customers or optimization of internal operational processes.

Systems integrators and cloud providers

R3 partners with the world’s leading global systems integrators (GSIs) who are engaged by their customers to leverage blockchain technology to tokenize assets and connect siloed databases across multiple organizations and business processes, while reducing costs. Corda is available via all cloud providers.

DON’t JUST TAKE OUR WORD FOR IT

Discover how customers are using Corda

customer success story

First uncleared crypto derivatives trades executed on a regulated platform

R3’s flagship platform, Corda, played a major role by sharing trade data and collateral information, and moving collateral in real time, with security and appropriate transparency among counterparties, custodians, and other relevant parties.

Mark Brickell – CEO, Clearmarkets

customer success story

Atomic delivery versus delivery (DvD) of securities

We built HQLAX on Corda from the outset – and the new version of the platform will enable us to further future-proof our offering and provide the flexibility our customers need.

Guido Stroemer – CEO, HQLAX

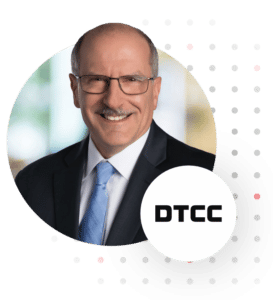

customer success story

Corda selected to power DTCC’s alternative settlement platform

Project Ion is an important step forward in advancing digitalization in financial markets and opens the door to exciting, new opportunities to drive greater efficiencies, risk management and cost savings for the industry.

Murray Pozmanter – Managing Director, President of DTCC Clearing Agency Services and Head of Global Business Operations

case study

Spunta—powering over 90% of the Italian banking sector (100+ banks)

Leveraging on the strengths of Corda, we brought full transparency to reconciliation activities, reduced operational risks and standardized the overall Spunta process. Through the continued collaboration with R3’s Professional Services and engineering teams, we moved from a pilot phase into production with the CorDapp, resulting in the Italian banking sector now using a DLT-based application to process everyday transactions.

Silvia Attanasio – Head of Innovation, The Italian Banking Association

FEATURED VIDEO

Project Dunbar—experimental multi-CBDC platform for international settlements

R3 has been a terrific and steady partner of MAS. We go all the way back to Project Ubin in 2016 and we are happy to have R3 take part in Project Dunbar along with Reserve Bank of Australia, Bank Negara Malaysia, South African Reserve Bank and Bank for International Settlements to test the use of CBDCs for international settlements.

Sopnendu Mohanty – Chief Fintech Officer, Monetary Authority of Singapore

cASe study

Instimatch Global streamlines unsecured money markets, FX and repo trades

Alongside R3’s large and impressive global ecosystem within the financial services industry, Corda is arguably the best–perhaps the only–real permissioned DLT, ensuring unparalleled confidentiality for the data residing on our platform.

Hugh Macmillen – Founder, Instimatch Global

AWARDS AND ACCOLADES

Industry recognition of R3’s commitment to enabling an open, trusted and enduring digital economy

Best Permissioned Technology Initiative of the Year 2023

Best Blockchain Technology of the Year 2023

CBDC Partner Initiative of the Year 2023

Most Innovative Use of DLT/Blockchain of the Year 2023

IBSi Global Fintech Innovation Awards

Most Innovative use of Blockchain in Banking of the Year 2023

Financial News

R3’s Chief Economist, Dr. Alisa DiCaprio named one of twenty ‘Most Influential Women in Crypto’ in 2023

Enterprise Blockchain of the Year 2022

Most Innovative Use of DLT/Blockchain

Best Use of Blockchain Technology

Best Use of Blockchain Technology

Financial News Trading and Tech Awards

Financial Technology Innovation of the Year 2021

Blockchain Product of the Year

Best Use of Blockchain in FinTech

Best Joint Venture for Spunta Banca DLT

Best Distributed Ledger Technology Provider

Financial News Trading and Tech Awards

Blockchain Initiative of the Year 2018

Ready to start building?

Be a part of a community that is building and shaping the future of finance.

"*" indicates required fields